")

")

")

")

Year LVII, 2015, Single Issue, Page 116

The TTIP: opportunities and risks

DAVIDE NEGRI

1. The background to the TTIP.

The economic crisis that began in 2008 has shattered the dream of creating a fully globalised economy: for years now the increasing strength of the BRICS group has prevented the WTO from going beyond the Doha Round. The impossibility of creating a single global free trade area leaves room for the coexistence of a number of macro-regions that are integrated to varying degrees.

The free trade agreement[1] currently being negotiated between the European Union and the United States, which seeks to gain leverage from the (fragile) superiority of the sum of the economic strength of the United States and the EU, can perhaps be seen as the most ambitious attempt yet to overcome the current impasse.

The USA and EU account for around 50 per cent of the global GDP and almost a third of global trade flows. USA-EU bilateral investment stock stands at 2.394 trillion euros, and goods and services worth an average of almost 2 billion euros are traded between these two areas every day. Thus, their progressive integration cannot fail to seem mutually advantageous.

In November 2011, on the basis of these premises, a body named the High Level Working Group for Jobs and Growth was instated, its task being to evaluate possible areas of collaboration between the two sides of the Atlantic. In December 2012, the Group presented an interim report that anticipated the conclusions of the final report, which was released in February 2013, just a few hours after the US president, in his annual State of the Union address, called for the start of negotiations for a free trade agreement between the US and Europe, to be called the Transatlantic Trade and Investment Partnership (TTIP). The report’s recommendations on the reduction andelimination of barriers to trade and investment concern a range of economic sectors. Particular importance is attached to the need to reduce technical barriers and enhance regulatory cooperation in order to strengthen convergence of standards and prevent new barriers from being introduced in the future.

The report identified three main areas on which negotiations should focus: 1) market access: elimination of tariffs and quotas for industrial products, agricultural products and services, liberalisation of investments, access to government procurement opportunities; 2) cooperation on regulatory matters: harmonisation of standards and removal of technical barriers to trade; 3) cooperation on global issues of common interest, in particular, the environment, employment, intellectual property, energy and SMEs.

In March 2013, the European Commission presented the Council with an impact assessment of the possible agreement. The document was based on previous studies and traced four hypothetical scenarios. However, the one emerging as most advantageous for both parties was that which envisaged a particularly aggressive programme of liberalisation, namely: total elimination of tariffs; 25 per cent reduction of non-tariff barriers (NTBs); 25 per cent reduction of barriers to services; 50 per cent liberalisation of public procurement. It is estimated that such a scenario would, over a ten-year period (2017-2027), allow the EU’s GDP to increase at an average annual rate of 0.48 per cent, which represents around 86.4 billion euros, while the increase in the US GDP would amount to 0.39 per cent, or 65 billion euros. At the same time, European exports to the United States would increase by 28.03 per cent (about 187 billion euros), while America would see its exports to the EU rising by 36.57 per cent (159 billion euros).

The agreement would also impact positively on world trade, generating an approximately 100 billion euro increase in global wealth. It is felt that this effect would be generated largely by the reduction of bilateral NTBs through greater regulatory convergence, which in turn would effectively result in an affirmation of global standards.

After nine rounds of negotiations (the most recent having taken place in April 2015), the European Parliament is now called upon to vote on the draft agreement, while in the United States Obama is struggling to push through Congress the changes needed to satisfy the Europeans.

The main aim of the present paper is to show how the TTIP represents, for both the Americans and the Europeans, an attempt to react to the growing geopolitical instability worldwide. In particular, the aim of the United States is to counter the loss of its hegemony in the economic-commercial field by joining forces with the countries that have historically been its allies. The EU member states, on the other hand, see the TTIP as an opportunity to secure a privileged commercial relationship with the world’s leading economy, negotiating with it on “almost” equal terms.

In Europe, however, the lack of a political body able to make decisions, together with the lack of a common foreign policy, is currently precluding the formation of a clear and precise common will. Instead, the illusion is perpetuated that it is more democratic to involve the 28 national parliaments, even individually, in the decision-making process – this would mean the agreement would need to be ratified in 28 different countries, in some cases through a referendum –, an argument that actually amounts to yet another attempt to defend national sovereignty in an increasingly fast-moving and volatile world in which, instead, the evolution of the economy needs to be governed more strongly and from a continental perspective.

2. From the globalised economy to the birth of regional economic networks.

In the post-Lehmann Brothers world, globalisation (or, rather, semi-globalisation) no longer exists in the form in which we once knew, admired and feared it: what we have today is a surrogate, a form of globalisation organised on the basis of regional networks, in other words, a sort of “economic regionalisation”.

When the WTO member states, with the sole exception of the developing countries, opened up their markets they laid the foundations of economic globalisation. But since then, the WTO has not succeeded in pursuing a true multilateral free trade agreement. In fact, the Doha programme has ground to a halt.

The economic and financial crisis that started in 2008, originating in the USA and then spreading to the rest of the world as an effect of the extremely high level of financial market integration, was stemmed only thanks to the states’ direct intervention in the economy through costly bailouts and support actions that increased the level of public debt. As we know, the crisis in the private sector was attenuated thanks to the states taking on the burden of the damage caused by the excessive deregulation of the financial system that had been part of the reason for the creation of the credit bubble.

Within this context of strong public intervention, the states used all the instruments at their disposal to help their economies. However, the problem is that the level of international cooperation that would make it possible to impose a balanced and far less confrontational course of action – in other words, so-called global governance of the economy – continues to be lacking. Moreover, it is globalisation itself that, by allowing new geo-economic players to enter the world stage, created the causes of its own downsizing. The BRICS countries, plus a group of 15 nations that are rapidly shedding the status of developing countries, need to find adequate economic space in order to grow. As a result, the old economic order based on large international institutions largely led by the United States and, to a lesser degree, its European and Asian allies (World Bank, WTO, International Monetary Fund), is no longer able to issue recommendations to new geopolitical players with the same efficacy as in the past.

In this setting, both the advanced and the emerging countries, in order to boost their own economies, make use of all the economic policy instruments available to them, namely:

1) competitive (currency) devaluation. This is a process that began with the Federal Reserve’s policy of quantitative easing and was subsequently taken up by all the advanced economies, such as Switzerland, the UK and, most recently, Japan (and the eurozone). Obviously, it has to be remembered that the emission of dollars presents no risk to the US economy, since the dollar is the reference currency in international trade.

2) The creation of new NTBs[2]. Unlike tariff barriers (currently prohibited by the WTO), NTBs have increased in number; moreover, they are a far more insidious form of protection as they use regulations, certifications, customs and control procedures and authorisations as a means of increasing import and export costs.

3) Privileged access to selected and complementary markets through the signing of free trade agreements between states, or between groups of states and others.

4) The use of soft and hard power tools in international affairs. This is a practice both of emerging countries and of advanced countries (the USA above all).

We are thus witnessing a gradual movement towards a world characterised by more marked divisions between geographical areas in competition with each other – a world in which preferential trade agreements are tracing new economic boundaries and spheres of influence. Each of the areas created is an expression of the power of geopolitical influence wielded by the dominant player in the region. It is no coincidence that the United States has, for some time, also been negotiating an agreement – the TPP (Trans-Pacific Partnership) – with the main Pacific Rim countries. At the same time, China, which is the only Pacific Rim country not included in the TPP negotiations, has been negotiating the FTAAP (Free Trade Area of Asia Pacific) with the very same countries, its intention clearly being to create an Asian economic community that has China at the forefront and from which the United States is excluded[3].

3. The strategic choices of the United States.

The financial crisis finally prompted the ruling class in the US to abandon the idea that American economic growth could be driven solely by the financial and housing sectors, while the manufacturing sector is recklessly neglected. Furthermore, also as a result of the loss of millions of jobs, especially in the service sector where there is less trade union protection and greater exposure to economic shocks, an economic orientation in complete contrast to the economic theory professed in the years leading up to the crisis has now begun to prevail in the USA.

Faced with the fact that it had proved unrealistic to think that the global economy could go on becoming more and more open, America’s ruling class saw that there was a need to revive investments in the manufacturing industry. In this regard, a study by the Interindustry Forecasting Project at the University of Maryland, seeking to establish whether the impact of the manufacturing industry in the US economy – it currently generates around 11.6 per cent of GDP – could return to the level (around 15 per cent of GDP) recorded in 1998, i.e. before the sector was hit by the wave of global recession, highlighted the profound changes in the structure of supply and demand that would be needed in order to achieve such an increase in added value, i.e. equivalent to around 4 per cent of GDP. Briefly, the following conditions are necessary to bring about a revival of the US manufacturing industry: 1) more exports and fewer imports; 2) a lower rate of price growth and more energy resources compared with current levels; 3) fewer regulatory requirements and corporate taxes in order to promote increases in production, investments and revenue (in all the other sectors too); 4) faster productivity growth in major service sectors, particularly the healthcare, construction, financial and trade (wholesale and retail) sectors, in order to meet workforce redeployment needs.

The model developed envisages a scenario in which, between now and 2025, the manufacturing industry would grow to 15.8 per cent of GDP and, in the same period, the sector’s total turnover would amount to 1,500 billion dollars, a figure representing a 49 per cent increase on current values, while personal savings and personal income would increase, and private consumption decrease. In this setting, over 3 per cent of GDP (including the capital investment share) would be diverted from services to the manufacturing sector.

But all this will be possible only if the US manufacturing industry is able to assert itself on the international markets. The model predicts an 8.2 per cent annual growth rate of exports; given that this parameter has stood at 7.8 per cent since the start of the recovery, all that is needed is a small increase, and in the context of the gradual strengthening of the global economy, this is a target that appears within easy reach.

Another growth factor is the energy boom now under way in the country. The policy of cutting energy costs is advantageous for all producers, especially those operating in energy-intensive sectors such as the chemical and metallurgical industries. Furthermore, the US government has authorised three new LNG export terminals, and exports of refined products such as diesel fuel are also likely to increase, especially if – as announced – projects for the conversion of natural gas into diesel fuel go ahead. Furthermore, in the “manufacturing revival” scenario envisaged, the production of natural gas would increase by barely 2.9 per cent a year, which is far lower than the growth rates recorded recently in this sector. What is more, the impact of the increase in oil production (which, at the very least, is destined to reduce imports and drive a growth in exports of refined products) is probably underestimated. As of now, the USA has around 130 thousand shale gas wells, mainly concentrated in the North East of the country. When the USA decides to export shale gas to India and China, this will undoubtedly pass via Europe and the Mediterranean, and this will pose a considerable threat to the European petrochemical industry. Moreover, the significance of shale gas does not end there: indeed, being available at such low prices, it is not just an instrument that lowers energy costs, but also a way of creating difficulties for countries that have built their fortunes on petrodollars and gas dollars, and thus of threatening the positions of countries not aligned with US policy (Russia, Venezuela, Iran, for example).

Internally, the USA is implementing aggressive measures to boost the revival of its manufacturing sector, such as the adoption of a local tax system and special taxation for companies. But revival of the manufacturing industry is an objective whose achievement also depends, to a large extent, on a strengthening of economic growth, compared with the results recorded following the start of the recovery, in the countries that are the USA’s main trade partners – particularly the EU, Japan, China, Mexico, Brazil, India and the four Asian tigers. Trade policy therefore plays a key role: indeed, it is only by finding outlets in new markets and ensuring the application of existing international standards that a country can increase the level of its exports.

The intention, therefore, is that the TTIP should serve as the foothold for gaining access to the mature markets on which the high-added value, high-tech goods produced by a newly thriving American manufacturing industry can be placed. Accordingly, the sectors most involved in the TTIP are the chemical and metallurgical industries, the aerospace industry (only in part) and the automotive industry. Shale gas and shale oil should become part of the agreement at a later stage, a development facilitated by the crisis in Ukraine and the instability in political relations with Russia.

4. Who in Europe really wants the TTIP?

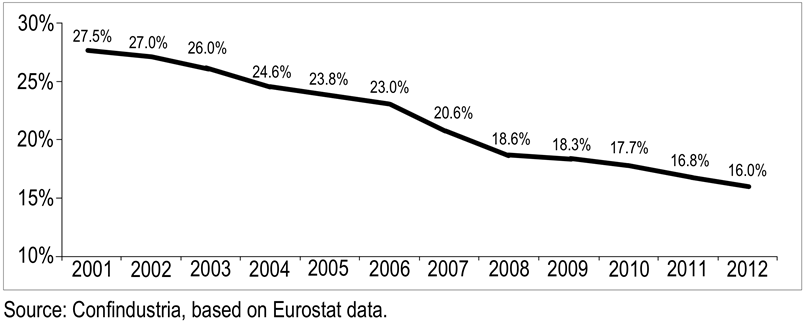

Even though the European Union and United States continue to hold the largest shares of global trade and investments[4], trade between them has declined over the past two decades. This decline can only be explained as a cumulative effect of various factors, such as the affirmation of emerging markets as new destinations for European and American exports and the impact of American NTBs (the various “buy American” provisions), although it should be pointed out that the dense web of transatlantic intra-company trade relations is not reflected in the official statistics on foreign trade.

Figure 1 – US share of total EU exports (2001 – 2012)

Even taking this last point into account, the decline in bilateral trade flows remains substantial and many commentators interpret the TTIP as a last-resort attempt to reverse this negative trend.

The growth of the global economy has come about, thanks to globalisation, through the development of long value chains, in other words, through the fragmentation of the whole process of research and development, engineering, production (manufacturing), distribution, logistics, marketing and customer services. Free trade agreements, when they involve economies in close geographical proximity to each other, allow exponential growth of value chains, especially in the manufacturing sector[5]. That said, it is easy to see that the TTIP strongly encourages the relocation not so much of production and manufacturing (given the equivalent cost of labour in Europe and in the USA), but rather of the upstream and downstream activities in value chains, such as research and development (and related intellectual property rights) and the functions and services associated with the final stages of the chain (from marketing to customer services, logistics and distribution). Indeed, if we examine the objectives declared in the official documents, it is possible to see that less importance is attached to tariff than to non-tariff protectionism. As regards the former, given that tariff levels currently stand at an average of around 3 per cent, the lowering of tariff barriers is an issue that really applies only to agricultural products. Instead, negotiations on non-tariff measures concern the convergence of regulatory standards, the improvement of protection of foreign investments, and access to the services, supply and procurement markets.

In short, we are faced with a free trade treaty in which what is being pursued is not so much “access to the goods market” – this is already largely guaranteed by the low level of tariff protection – as an agreement concerning both investment protection and liberalisation of services. In fact, what both parties are wanting and hoping to obtain is the possibility of relocating adequately protected systems and technologies connected with the liberalised exchange of goods and services.

How does European industry stand to benefit? According to a recent study by the European Parliament’s research service published in January 2015[6], the sectors that will benefit most from the TTIP are – considering the ambitious liberalisation scenario – motor vehicles (+148 per cent), metals and metal production (+68.2 per cent), processed food (+45.5 per cent), other manufactured goods (+22.8 per cent), chemicals (+36.2 per cent), electrical machinery (+35 per cent), other transport equipment (+25.5 per cent), wood and paper products (+19.9 per cent).

These figures seem to suggest that Germany, given its industrial tradition, stands to benefit the most. But in actual fact, the TTIP, by reducing the bureaucratic procedures that previously represented fixed costs, will also support the industrial fabric of countries where SMEs are the backbone of the economic system: indeed, it is forecast that Sweden, Finland, the UK, Ireland, Spain, Bulgaria, Cyprus, Greece, Malta and Latvia are the countries that will benefit most from the TTIP.

The main concerns of European industrialists are being voiced in energy-intensive sectors such as the steel, chemicals, cement and paper industries, where operators fear that their products may become less competitive as a result of the lower cost of American energy generated from shale gas and shale oil.

As a further consideration, it can be noted that half of USA-EU trade concerns value chains that are controlled by networks of medium-sized and large enterprises and transnational groups, and that the SMEs will benefit along with them: indeed, being subcontractors to large industrial groups they will enjoy the benefits of the new trading opportunities open to the latter.

A final point worth noting, given that public opinion at European level is often absent, dormant or divided between the different nations, is that the TTIP is a topic that has contributed to the formation of a “European” public opinion. When a broad debate evolves at the level of public opinion, with expressions of either support for (through agricultural producers’ and industrial manufacturers’ associations) or opposition to (through consumer associations and various political parties) a given treaty, it results in the exercising of greater control, which in turn confers greater legitimacy on the work of the European institutions. This is the only possible explanation for the fact that many previously confidential documents relating to the negotiations have now been made public, and also for the desire to make both the debate in the European Parliament and the current negotiations as transparent as possible. This debate is helping to increase the member states’ awareness that singly they are not in a position to negotiate with large countries (like the United States, but also Russia, China and India), and that they need the European dimension in order to express a single political will (only one) and, in so doing, act with more responsibility on the world stage.

An example of all this is provided by the Bernd Lange’s report (S&D, Germany) on the TTIP[7], which, were it to be approved, would send out a strong political signal that the Commission would have to take into account in further negotiations. Thanks to the report some mediation proposals have been drawn up on the most debated and controversial topics, which include the so-called ISDS (investor-state dispute settlement) system. The proposed solution is to create an international court of investments whose work would be made public and whereby a mechanism of appeal would be provided for, the consistency of judicial decisions would be guaranteed, and the jurisdiction of European courts and the member states would be respected.

5. Final considerations.

While the TTIP presents the EU with important objectives and, above all, has considerable strategic value, the Europeans nevertheless need to be aware that “more trade” does not automatically mean “more growth” and that the latter depends on the existence of a decision-making centre able to implement appropriate policies for growth. Free trade is, as we know, a great opportunity offered to everyone, but it is an area in which the better prepared are often the ones that benefit the most. If the Europeans truly want to exploit to the full the creation of the world’s largest free trade area, they must complete their political integration and thus ensure that the continent’s economy can count on a solid and coherent control room for the coming decades, just as the United States can. Otherwise Europe is destined to remain trapped by the need for a unanimous vote in order to implement any decision. The TTIP itself is an emblematic case in point. It can be approved through two possible avenues: the first is to consider the TTIP a mixed agreement, wherein the Union and the member states share responsibility for ratifying the treaty, which means there must be a ratification procedure in each of the 28 member countries (with the added risk that some of these might opt for a vote by referendum with all its attendant consequences); alternatively the TTIP can be considered exclusively a competence of the European Union, and thus as a non-mixed agreement whose ratification requires only a qualified majority vote in the Council and the European Parliament. And at this point there arises an institutional paradox: it will take a unanimous vote in the European Council in order to opt for the non-mixed state agreement solution; if this is not achieved – there need be only one vote against – then it will be necessary to go down the route of ratifying the TTIP in each of the 28 member countries.

[1] Free trade agreements are a means of creating strong economic links between states by removing, as far as possible, barriers to the exchange of goods and services between economies through regulation of the “rule of preferential origin” of goods, which, in turn, is a means of determining when a given commodity can be considered a product of a given country.

[2]Reference should be made to the Commission’s 2012, 2013 and 2014 reports to the European Council on barriers to trade and investment.

[3] On 10 November 2014 during the APEC summit in Beijing, the Chinese president illustrated his “Asia-Pacific dream”, namely his vision of a free trade area that together with free trade agreements and investment opportunities will provide funds for infrastructural investments that will connect East Asia with Europe: the Silk Road and Maritime Silk Road initiatives.

[4] EU: 25.1 per cent of world GDP and 17 per cent of world trade; USA: 21.6 per cent of world GDP and 13.4 per cent of world trade.

[5] One might think, for example, of the recent free trade agreements between the EU and the countries of North Africa and Eastern Europe, or with Turkey (with which a customs union agreement is in force), which have made it possible to create large manufacturing areas and allowed the relocation of Italian, French and German enterprises to those countries.

[6] TTIP impacts on European Energy Markets and Manufacturing Industries, IP/A/ITRE2014-02, study provided at the request of the Industry, Research and Energy Committee of the European Parliament.

[7] The vote on the Lange report, initially scheduled for June 8, was postponed to allow consideration of the large number of proposed amendments.